Markets have been buying into the LTRO like there's no tomorrow, while blogosphere and bank research has been medium-term negative in its comments - especially as oil prices have rallied in tandem. Is this a proper risk-on, as the last time I remember similar market cointegration was in 2008? A case of buy the rumor, sell the news? The three charts beside Euro Crisis: General tell the whole story - debt outside the eurocore unsustainable, credit crunch and slow-motion deposit-run from the periphery to the core. The game is still very much on.

Two of my previous calls were JPYUSD and EURUSD. JPY already did what I said it would do, we will see about the EUR tomorrow. I am on Twitter, Facebook, email and paper.li

News – Between The Hedges

Markets – Between The Hedges

Recap – Global Macro Trading

EZ crisis press summary – openeurope

Debt crisis: live – The Telegraph

Europe Crisis Tracker – WSJ

EURO CRISIS: GENERAL

A Euro Sabbatical – Project Syndicate

Hans-Werner Sinn: Those crisis countries that do not want to take it upon themselves to lower their prices should be given the opportunity to leave the eurozone temporarily in order to devalue prices and debts.

Giles Merritt: Electing the EU’s leaders is one thing; introducing greater accountability will be quite another. Nobody knows which rules and procedures would alter the widespread view that “Europe” is run by faceless mandarins who are immune to criticism or sanctions, but a move in this direction is urgently needed to safeguard the EU’s credibility.

Giles Merritt: Electing the EU’s leaders is one thing; introducing greater accountability will be quite another. Nobody knows which rules and procedures would alter the widespread view that “Europe” is run by faceless mandarins who are immune to criticism or sanctions, but a move in this direction is urgently needed to safeguard the EU’s credibility.Capital Flight From Italy, Greece, Portugal Accelerates; Two Trillion Fantasy; Merkel Weaker Every Week; Crude and Geopolitical Risks – Mish’s

That Portugal enigma, demystified – alphaville / FT

That Portugal enigma, demystified – alphaville / FTCitigroup explains Portugal is not fiscally sustainable: the size of the haircut will need to be raised to 50%... assuming that market access cannot be regained before 2016, Portugal would need an extension in its official funding of between €50bn to €65bn.

Martin Feldstein: If this is the essence of the fiscal compact that is eventually agreed, it will have no predictable effect on eurozone countries’ behavior. Its only effect will be to allow the eurozone’s political leaders to claim that they have created a fiscal union, and thus that they have moved Europe closer to the political union that is their ultimate goal.

Podcasts:

Saxo Bank’s Beecroft Says Europe Has ‘Many Hurdles’ – BB (mp3)

Foley Says European Crisis ‘Alive and Kickin’ – BB (mp3)

ICMB’s Wyplosz Says Greece, Italy & Portugal to Default – BB (mp3)

In the Balance: A Marshall Plan for Greece? – BBC (mp3)

In the Balance: A Marshall Plan for Greece? – BBC (mp3)

Join Stephen Evans in Berlin and guests: Richard Parker from Harvard,a former advisor to the Greek prime minister; Peter Bofinger, a member of the German Council of Economic Experts;Irwin Collier of the Free University in Berlin and Christos Katsioulis of the think tank the Friedrich Ebert Foundation. Along with resident comedian and ex management consultant Colm O Regan in Dublin.

EURO CRISIS: GREECE

Interestingly, the central bank’s holdings include about a third of the famous €14.5 billion Greek bond due to mature on March 20, the one that everyone was worried about… In order to keep the ECB out of the restructuring, Greece gave the ECB fresh new bonds this month in exchange for the bank’s holdings. Then, Greece restricted the restructuring to bonds issued prior to 2012.

Whatever happens to Greece, it is becoming increasingly difficult to pretend that the most unpleasant dealings with that economy—repeated bail-outs, private-sector involvement in debt restructuring, and missed deficit targets—will not be allowed to occur elsewhere.

Has Greece CDS been triggered? The question’s finally been posed to Isda’s determination committee and is currently pending

Burying parliamentary scrutiny? – openeurope

762 pages of Greek bailout agreement: how in the world are MPs supposed to fulfil their role scrutinising the decisions reached by governments. The bailout took eight months to organise, now MPs were expected to approve it with a weekend's notice (at least with respect to the details).

EURO CRISIS: ECB, LTRO

The (European) Placebo Effect – Peter Tchir / ZH

What is being ignored is evidence that banks are hoarding most of the LTRO cash for future debt repayment, growing concern that senior unsecured lenders to banks are becoming too subordinated by the ECB, changes in laws designed to hurt bondholders, growing concern over ECB’s SMP holdings – both as a form of subordination to other bondholders and a source of real risk to the countries backing up the ECB. Very little has been fixed and in fact progress has slowed down on some things.

What is being ignored is evidence that banks are hoarding most of the LTRO cash for future debt repayment, growing concern that senior unsecured lenders to banks are becoming too subordinated by the ECB, changes in laws designed to hurt bondholders, growing concern over ECB’s SMP holdings – both as a form of subordination to other bondholders and a source of real risk to the countries backing up the ECB. Very little has been fixed and in fact progress has slowed down on some things.LTRO 2 101: Top-Down – ZH

SocGen expects 300-400bn: The LTRO cannot be completely separated from another key event, just a couple of days later: the EU 1-2 March Summit. A large LTRO and a 50% increase to €750bn of the rescue mechanism would be 'risk-on' (would also make us heavy sellers of Bunds vs swaps)

LTRO 2 102: Projected LTRO Take Up By Bank – ZH

Draghi said there is no stigma trade. We proved him wrong, at least in the interim. LTRO 2 will finally decide who is right and who is wrong.

The euro, the L-throw – alphaville / FT

Views from Morgan Stanley and Credit Suisse, all their scenarios are either euro neutral or negative.

The “L-troh”, the credit crunch, and the carry trade – alphaville / FT

Views from Nomura, SocGen and RBC. Alphaville comments: this is more about propping up banks and ailing peripheral sovereigns…The increased uptake from Italian and Spanish banks is the real message though, and it looks like both will be back in force for round two.

How Banks Will Use This Week's 3-Year LTRO – BI

SocGen has a roundup of how banks -- through media reports and publicly stated intentions -- intend to use this operation.

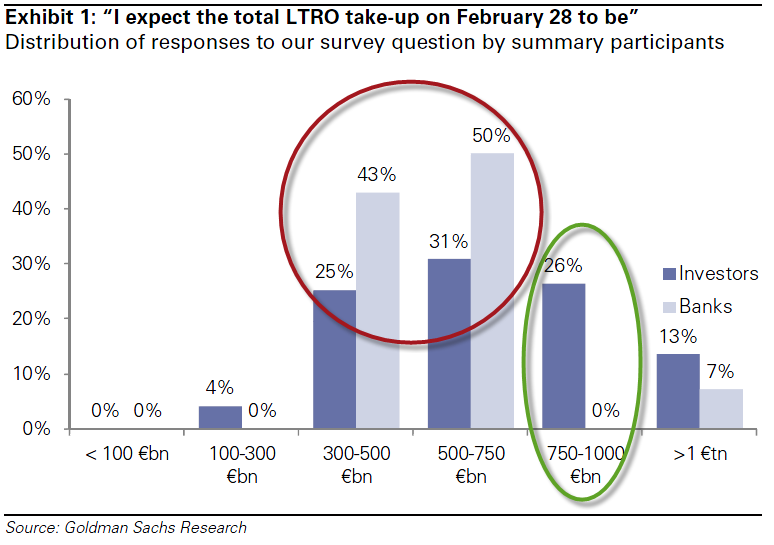

Here Is Why Someone Will Be Disappointed By The LTRO – ZH

Goldman Sachs surveyed its clients and found a gaping divide between banks and investors with the latter expecting considerably more than the banks - it seems someone will be disappointed - investors hope for more and banks expect to do less.

ECB wall of cash averts credit crunch – Reuters

The euro zone avoided a credit crunch in January but banks showed scant sign of lending on the funds they snapped up at the European Central Bank's first 3-year lending operation to companies which have been starved of investment funds.

RBS and Lloyd’s are considering borrowing… this is actually not new. RBS (€5bn) and possibly HSBC accessed the first LTRO back in December when there was little furore over the process and there has been little fallout since.

The only major U.K.-based bank to have so far ruled out accessing the next round of LTRO is Standard Chartered PLC. A spokesman for the emerging markets-focused bank said that it didn’t need the funding.

ENERGY

The EU oil consumption has been tightly linked to the region's GDP growth. The combination of these record energy prices for the EU (given weak currencies) with the Eurozone's credit crunch will significantly reduce EU's demand for crude in 2012.

UBS: To the extent that rising prices reflect stronger growth, price increases can be sustained—up to a point. For oil consuming countries, rising prices will begin to crimp purchasing power.

Game Changer – PIMCO

…cyclical support to globally traded commodities like oil…onshore natural gas shale and oil shale developments are creating opportunities to invest in energy companies that may grow significantly faster than the overall U.S. economy.

In the category of Best Additional Worry in a Globalised Economy – alphaville / FT

Signs of a hard landing in China, looming French elections, the prospect of rising sovereign bond yields, and the threat to oil supplies

The end game – Asia Times

The oil markets are completely manipulated and orchestrated, and the conductors of the orchestra have the benefit of having already held a rehearsal in 2008. History never repeats itself, but it does rhyme. This time around it is not demand from the United States that is collapsing, but European Union and United Kingdom demand, as oil prices in euros and pounds sterling have never been higher.

Oil at $150? – Capitalists@Work

Politically the showdown with Iran has to come sooner or later, although an Arab Spring type event would be much more welcome. Economically, we just can't afford it in the next 3 years.

OTHER

Goldman and Stratfor planned a trading operation– alphaville / FT

From Wikileaks / anonymous files.

The long-term or reversion to the mean – Buttonwood’s / The Economist

On Jeremy Grantham’s quarterly letter: full pdf

OFF-TOPIC

I walked very slowly. I was new here, a first-timer. That Wednesday, I was eager to hear Merkel, but on my way I got sidetracked in the lounge by conversations that seemed interesting, especially the ones I wasn’t part of. It was a name-dropper’s paradise.

The relational aesthetics of Davos – Felix Salmon / Reuters

Comments and adds to the above.

Good at Finance vs Good at Life – Interloper

I have no idea how to move the goal posts to allow more of “the better angels of our nature” to rise to prominent positions in finance, or even if it’s possible. I do believe, strongly, that the personality type that typically rises to the top of a global investment bank provides further evidence that the current control over legislation enjoyed by the financial lobby should be brutally curbed.