FED asks when they will raise the interest rates in US, and is there any more QE coming looks at the inflation picture in US and debates when the monetary policy will tighten again. OIL is related to the Fed, as the economies cannot sustain much higher prices, but unfortunately the easy monetary policy, competitive devaluations and epic policy fail in Middle East have pushed the price high. Since when have stocks, gold and oil rallied together? Answer in the attached video...

The OTHER has some interesting gems, including Warren Buffet's latest annual letter, this week's must-read even without looking. OFF-TOPIC ends this massive post with articles that are actually interesting and help you forget about how little intelligence the world is ruled with.

EURO CRISIS: GENERAL

Harold James: Banking and budget problems, fiscal constraints, and the emergence of “non-political” technocratic governments: all are horribly familiar to Germans with a sense of the past

European Crisis Realities – Krugman / NYT

The stories that excessive welfare state or budget deficits are behind the crisis are false – it is a current account crisis. The current medication tries to cure the symptoms, not the disease.

Solidarity within the Eurozone: how much, what for, for how long? – Notre Europe (pdf)

From a think-tank calling for more (temporary) solidarity. Use source criticism, but read it to understand the arguments of the “dark side”.

Faced with unpredicted recession, Spanish PM Mariano Rajoy said he will "talk to the EU commission" about easing the country's deficit target for this year.

Golden rule or golden straightjacket? – voxeu.org

Karl Whelan: Europe’s Fiscal Compact is being widely sold as the essence of prudent fiscal management. But this column argues that the rules in the Fiscal Compact severely restrict a country’s ability to use fiscal policy to stabilise its economy and will often require debt levels far below those considered sensible. The rules should be changed before they become a straightjacket.

With its ageing population—only in South Korea will the dependency ratio increase faster, says the OECD—Germany may be forced to speed up the reform process in order to raise the employment of women.

EURO CRISIS: ECB & LTRO

Draghi Says Continent's Social Model Is 'Gone,' Won't Backtrack on Austerity

ECB: LTRO II – Danske Bank (pdf)

We list a number of arguments favouring either a small or a large take-up at the second three-year LTRO on 29-Feb. We conclude that the allotted amount is likely to be between EUR300bn and EUR600bn. A smaller amount would cause sovereign spreads to widen, while a bigger amount would be likely to cause the most notable market reaction with a risk rally in many asset classes.

So long, covered bond LTRO carry-trade – alphaville / FT

Pretty attractive in December. Not so much now. That at least, is the view of Leef Dierks at Morgan Stanley

Next Week’s LTRO: Too Great Expectations? – MarketBeat / WSJ

RBS surveyed 160 bond investors and found on average the group expects next week’s take-up for the ECB’s money manna to be €574 billion. That would be an increase from the €489 billion hoovered up by banks in December. Expectations ranged from €201 billion to €1.437 trillion.

RBS surveyed 160 bond investors and found on average the group expects next week’s take-up for the ECB’s money manna to be €574 billion. That would be an increase from the €489 billion hoovered up by banks in December. Expectations ranged from €201 billion to €1.437 trillion.

|

| They have money for full-page ads? |

Greek statement on bond swap: in full – The Telegraph

Athens has launched a bond swap with private investors to slash €107bn of the country's debt. Here is the Greek statement in full.

A Bad Eurogroup Decision on Greece – PIIE

There are at least ten reasons why this agreement is wrong. So what should have been done instead? The European Union will have to revisit its bad decision of February 21 on the Greek crisis. The earlier it does so, the less the cost will be. The euro area needs to broaden the default but keep it amicable and to keep Greece within its membership. The trick is to treat the ECB, the European Union, and EU countries as private bondholders and make their own sacrifice deeper. The European Union should take more costs of the Greek crisis as defaults on bonds and offer less as assistance, or to be more specific as loans.

There are at least ten reasons why this agreement is wrong. So what should have been done instead? The European Union will have to revisit its bad decision of February 21 on the Greek crisis. The earlier it does so, the less the cost will be. The euro area needs to broaden the default but keep it amicable and to keep Greece within its membership. The trick is to treat the ECB, the European Union, and EU countries as private bondholders and make their own sacrifice deeper. The European Union should take more costs of the Greek crisis as defaults on bonds and offer less as assistance, or to be more specific as loans.

Greek CDS settlement auction is ‘lifeguards swim only’ – Sober Look

This settlement pertains to the Greek law bonds, while there is still uncertainty around €18.5bn of the UK law ("international") bonds. Other uncertainties remain as well, mostly associated with the actual process, given this unusual CDS settlement (vs. say corporate CDS whose settlement is commonplace.) By the time we get to Portugal or Ireland, everyone will be an expert.

If The Greek Bailout Is So Bad... – BI

Citigroup’s Steven Englander: what continues to strike me is how low baseline expectations are for the EUR and how all it takes is a bit of easing of tail risk to push it upwards.

Greek bail-out threatened by Germany-IMF stand-off – euobserver.com

Greece's second bail-out still faces hurdles as Germany and the IMF wait to see who moves first on financial commitments related to the deal.

This week Europe’s leaders faced a choice somewhat similar and perhaps equally momentous as America’s leaders faced in 1787. But this week they chose a path that looks punitive and short-sighted, pursuing European unification but likely to generate discord and eventually fragmentation. Seldom does one act determine the future, but they might find it difficult to undo what’s been done this week. The only certain result is much suffering and humiliation for the Greek people. We can only guess at how this will work for Europe as a whole

The Greek rescue – an agreement that few believe – Comstock Partners / Pragmatic Capitalism

Even the assumptions underlying the IMF’s base case is incredulous. To get Greek government debt down to 120% of GD:P by 2020, they assume no GDP growth this year and an average of 2.6% annually for the following seven years. Does anybody in his right mind really believe this is possible with higher taxes and drastic cuts in government spending, wages, pensions and employment?

Why should any international investor of any type purchase debt with a CAC issued by the Greek government, where the ability to adjudicate a dispute with the government of Greece is in the courts in Athens?... We know that, at inception, moral hazard cannot be priced in the markets. As we learned from Lehman Brothers, a primary dealer of the Federal Reserve, moral hazard’s cost is only measurable after the fact.

Greece Issues Exchange Offer Terms; Raises Minimum Acceptance Threshold To 75% From 66%; €10 Billion Buys PSI Killer – ZH

UK law bonds of just €29 billion are part of the deal, and one can buy a blocking stake there, at roughly 30 cents on the euro, for a meager €2 billion in cash out today. Furthermore since many hedge funds already have built up blocking stakes, this almost certainly means that Greece will not get the requisite needed votes to pass the exchange.

If you go to the official website for the Greek bond exchange, greekbonds.gr, you can now find an actual official document! The rest of the website, it says, “will be available shortly”, whatever that’s supposed to mean.

The worlds inside a Greek GDP warrant – alphaville / FT

Greece issues them attached to the new bonds but you can detach them for trading around. They have the same notional value (31.5 per cent). Payments come if, and only if, Greece’s nominal GDP level is above “a defined threshold” AND the GDP growth rate continues above a “specified target”. The formal PSI release contains neither definition nor specification. So far. Your mind drifts back to Argentine official inflation stats…

Greece issues them attached to the new bonds but you can detach them for trading around. They have the same notional value (31.5 per cent). Payments come if, and only if, Greece’s nominal GDP level is above “a defined threshold” AND the GDP growth rate continues above a “specified target”. The formal PSI release contains neither definition nor specification. So far. Your mind drifts back to Argentine official inflation stats…

the full release doc — we’re still waiting for the technical memo stuff

That Greek sustainability analysis, annotated – alphaville / FT

Gary Jenkins of Swordfish has an early draft with some revealing scrawlings…

FED

Guess which US bank holds assets equal to a fifth of US GDP and half of it in extremely long maturities (10+ years)?

Inflation Expectations & Stocks Still Moving In Lockstep – The Capital Spectator

My guess is that when the crowd believes that economic growth is sustainable without extraordinary support from the central bank, the new abnormal will fade. At that point, inflation expectations and the stock market will go their separate ways, which is the historical norm.

Those believing the Fed is on hold for the next 3 years… – Sober Look

The Fed Funds futures have the first rate hike (25bp) centered around August of next year and the second hike (to 50bp) on July of 2014.

Monetary policy: When will the Fed hike rates? – Free exchange / The Economist

The market is not pricing in an early rate hike. It's following the Fed's guidance.

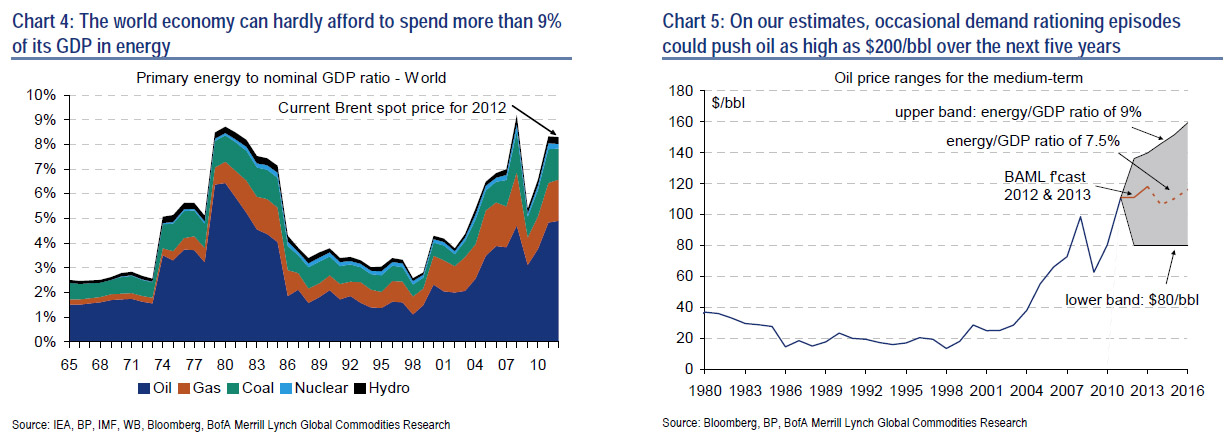

OIL

|

| Click to enlarge. Oil is expensive, and soon maybe more so. |

America now imports 15 percent less foreign oil than it did in 2005. Yet prices remain stratospheric, thanks to healthy demand overseas and the tense situation in the Middle East (Libya last year, Iran this year). And so, even with imports falling, the United States still paid more for foreign crude in 2011

$200 Oil Coming As Central Banks Go CTRL+P Happy – ZH

Bank of America: oil prices to remain a key constraint on global growth, world can hardly afford to spend 9% of GDP on oil. Supply constrained and increased liquidity should set oil prices on upward path.

What Rising Gasoline Prices Do to the Economy – of two minds

Charting gasoline prices against income and GDP provides some interesting results.

OTHER

The State of the World: A Framework – Stratfor

George Friedman: Three major areas of the world are in flux: Europe, China and the Persian Gulf. Every country in the world will have to devise a strategy to deal with the new reality, just as 1989-1991 required new strategies. The most important country, the United States, had no strategy after 1991 and has no strategy today.

Frail Fundamentals, Rising Liquidity: Where to Invest? – EconoMonitor

Capital preservation via a defensive asset allocation is priority. Over the next couple of years, cash could work as both an insurance against sharp downturns and the required seeding-capital to quickly size opportunities. Still, in the longer-run keeping liquid portfolios will result in low returns.

G20: Little Scope for New Initiatives – Credit Writedowns

three key issues: IMF funding, replacement for Zoellick, who will step down as head of the World Bank, and the oil shock. It is unlikely that any of these issues are resolved at this G20 meeting. However, important groundwork could be laid for future decisions.

Breaking Ranks: Former Broker Turns Bomb Thrower – AdvisorOne

Joshua Brown is a reformed broker and thinks you should be one too — or else.

We read so you don’t have to: Tax policy lessons from the OECD – Wonkblog / WP

Corporate taxes are found to be most harmful for growth, followed by personal income taxes, and then consumption taxes.

Corporate taxes are found to be most harmful for growth, followed by personal income taxes, and then consumption taxes.

Nanosecond Trading Could Make Markets Go Haywire – Wired

“There’s this whole world below 650 milliseconds. It’s like landing on another planet,” said Neil Johnson, a complex systems specialist at the University of Miami and co-author of the study, released Feb. 7 on arXiv. “It’s an enormous part of the market which is out of human reach. We have a glimpse of the kind of ecology that’s going on down there.”

GMO Quarterly Letter Feb 2012 – ZH (pdf)

Your Grandchildren Have No Value (And Other Deficiencies of Capitalism)

Andrew Lo – Wealth Track (mp3)

Managing your portfolio’s risk in volatile times with “Financial Thought Leader,” MIT professor and alternative money manager Andrew Lo.

Drowning in High Water Hell? – Pension Pulse

But now it's hedge funds that are reeling, drowning in high water marks. My advice? Unless you have deep and patient pockets backing you up, walk away, it's simply not worth it. When you see the head of Goldman's hedge fund group retiring, you know it's time to call it quits.

OFF-TOPIC

How Companies Learn Your Secrets – NYT

William Gibson on Cultivating a “Personal Micro-Culture” – brain pickings

On the building blocks of creativity and acquiring a sense of what feels right.

The Commission takes transparency too far... – openeurope

Olli Rehn asked about his dress code in sauna

Teller Reveals His Secrets – The Smithsonian Magazine

The smaller, quieter half of the magician duo Penn & Teller writes about how magicians manipulate the human mind

Book Bits For Saturday – The Capital Spectator